Changing tides for 529 market and its investors

The tax advantages and provisions associated with 529 accounts have continued to evolve since their introduction in 1996, but they are by no means a "new" savings vehicle.

Yet we continue to see an impressive growth trajectory, with over 450,000 new 529 account enrollments in 2019.

456

,

895

new 529 account enrollments

$

3

,

807

average initial contribution amount for a new account

4

,900,000+

total 529 accounts on our platform

529 balances shift in sync with market performance

The overall average 529 account balance has grown by 28% over the past five years, which represents a 17 percentage point jump in the five-year rate relative to 2018. This overall average balance also increased by almost $3,000 in 2019, as the market recovered after some fluctuations in late 2018. It's important to keep in mind that a 529 account is a long-term savings vehicle that's ultimately designed to enable savers to recover and grow earnings with market corrections and upticks.

$25,665

overall average 529 account balance in 2019

28%

increase in average 529 account balance since 2015

529 Average Account Balances

How much progress have 529 savers made?

As we've noted, 529 balances increased year-over-year across all account owner age ranges. But savers ages 25 to 34 saw the most dramatic jump in their average balance in 2019, with a 20% increase over 2018. Savers ages 35 to 44 and 55 to 64 saw a very similar year-over-year increase in education savings of 16%. Not surprisingly, savers ages 45 to 54 who have had a longer time horizon to save than their younger counterparts and likely have beneficiaries approaching college age had the highest overall average balance at $35,327.

Average 529 Account Balance

529 Mythbusters: Savings Aren't "trapped"

Feedback from real savers makes it clear that some individuals fear what might happen to their 529 savings if their financial situation or their child's education plans change. Is it even possible to tap into those savings for uses outside of education expenses? Or, will the penalty for making a non-qualified 529 withdrawal be too steep to swallow?

To clear this up, we took a look at actual withdrawal behaviors for qualified and non-qualified distributions during the 2018 tuition payment season.1

How much education buying power did our 529 savers have this year? And, what happened to the 1% of savers who did opt to make non-qualified withdrawals?

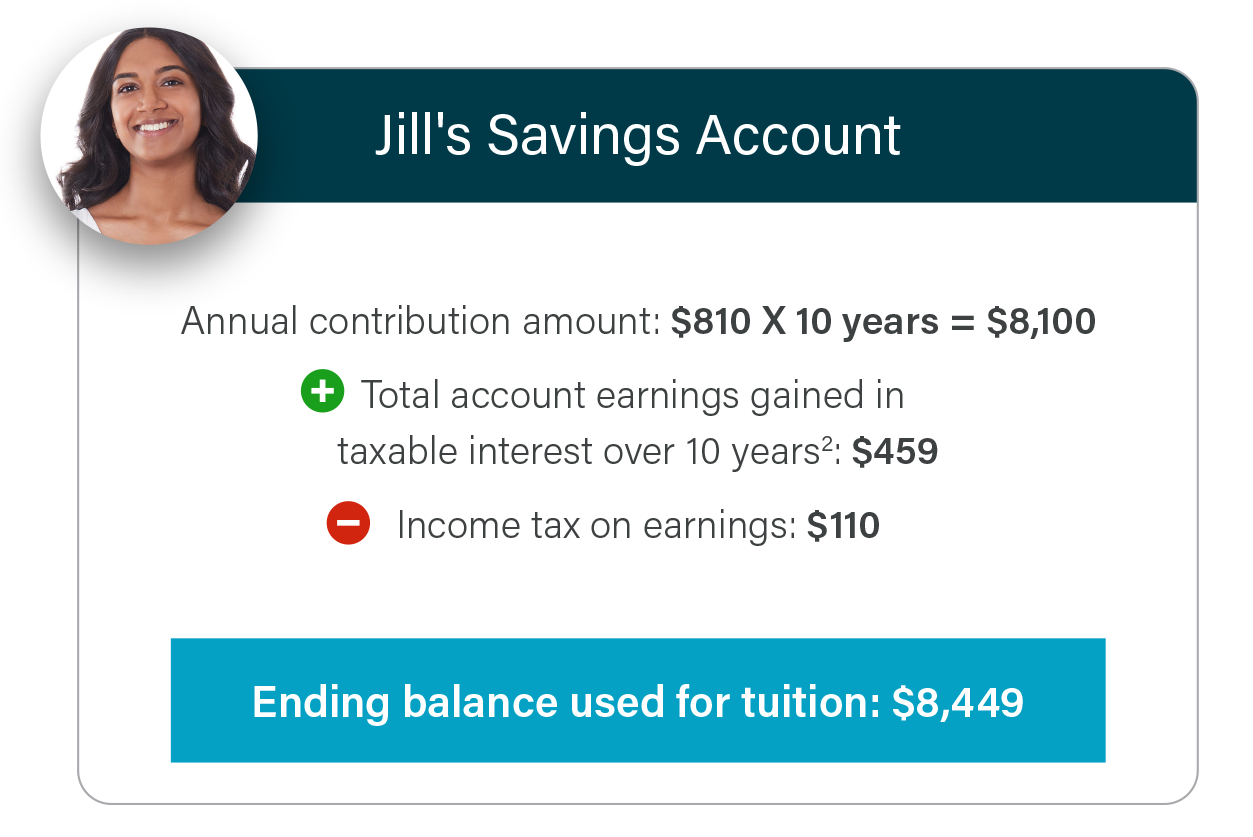

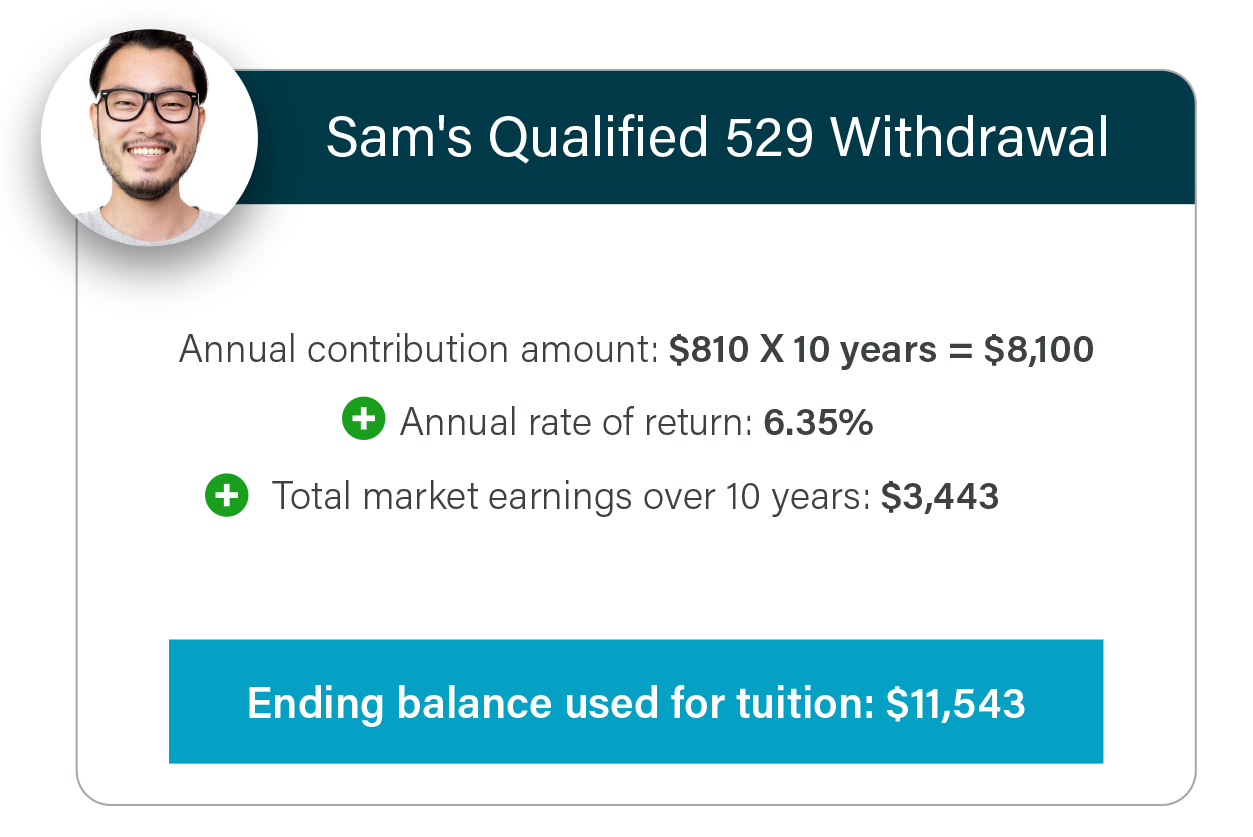

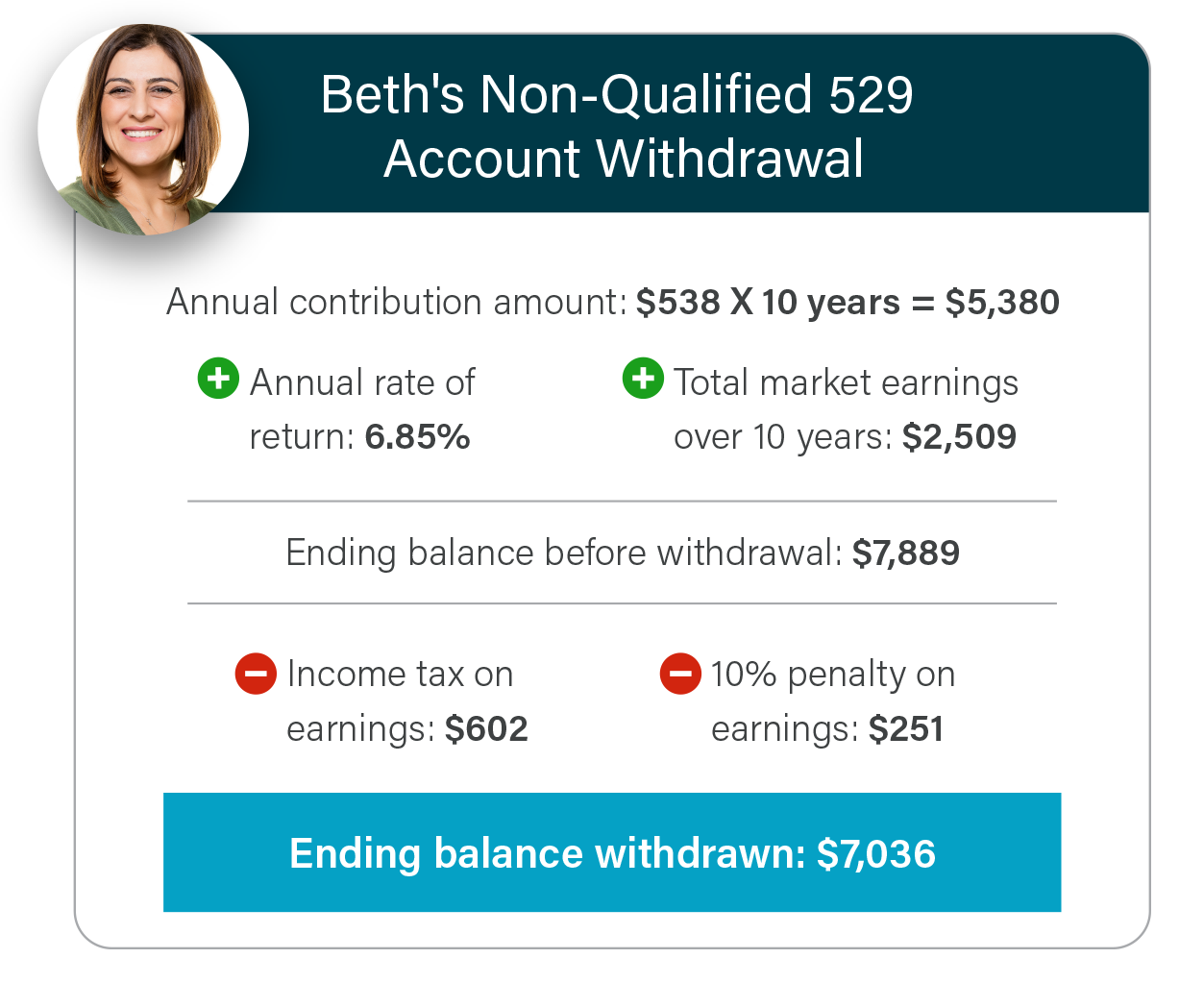

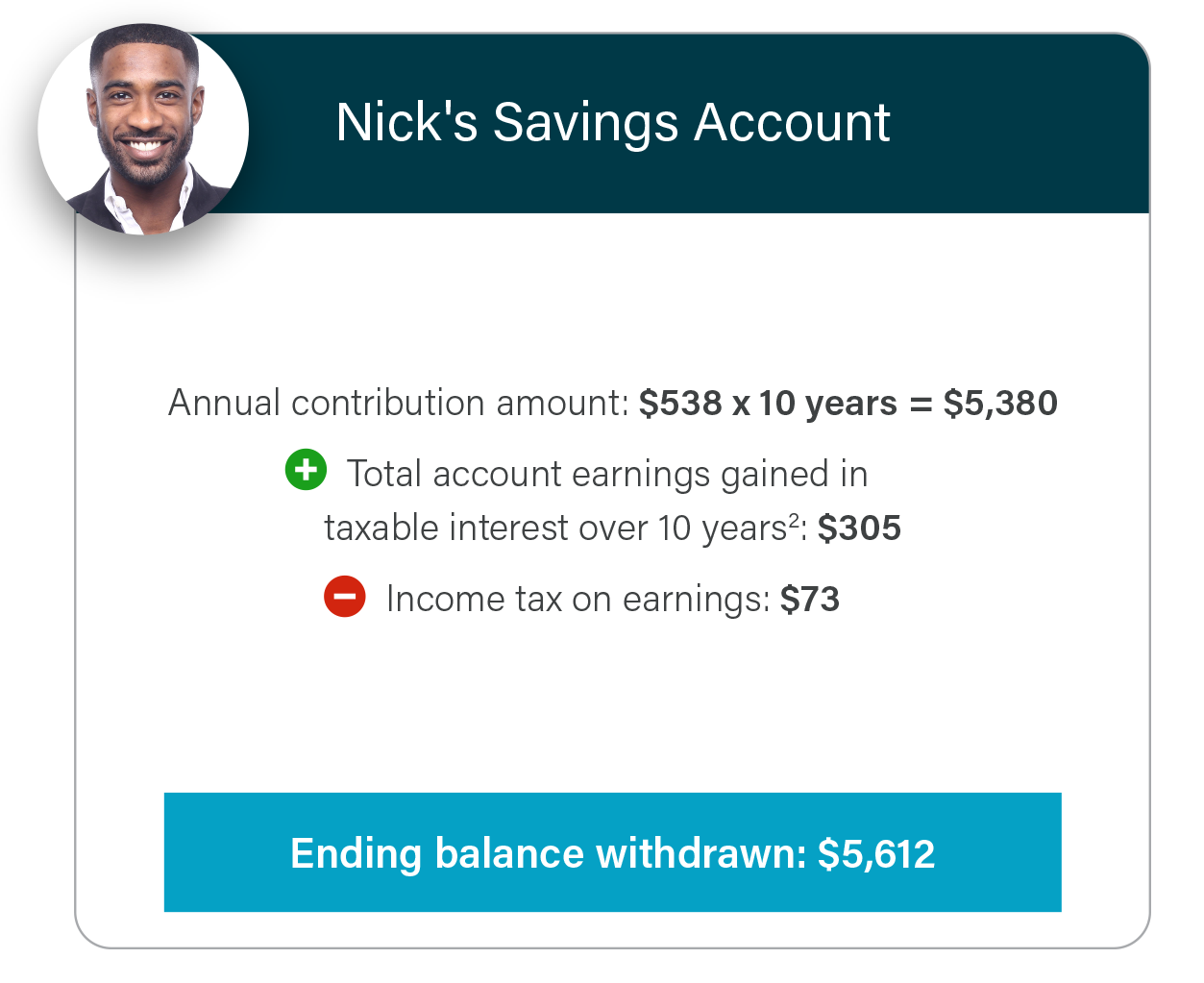

Consider the savings journey of these 4 individuals, who each started saving for education 10 years ago:

How did these savings journeys differ?

From these hypothetical calculations, Sam saved $3,094 more than Jill to use toward education expenses by investing in a 529.

From these hypothetical calculations, Beth is still $1,424 better off than Nick by saving in a 529 account, even after paying the penalty for a non-qualified withdrawal.

The bottom line?

By choosing a 529 account over a more standard savings structure, you can potentially make your annual contributions work that much harder for you and your account beneficiaries. The vast majority of our savers find themselves using their 529 to directly fund education, but there's still a path for those who might need to leverage these savings for other priorities.

1 Based on $4.3 billion in qualified withdrawals, with a rounded average investment amount of $8,100 and $52 million in non-qualified withdrawals, with a rounded average investment amount of $5,380 over 10 years.

2 Interest rate calculated at 1% APY

Methodology The above analysis is based on aggregate data across account owners with account beneficiaries aged 17 to 22 who made qualified withdrawals between Jun 1, 2018 and January 1, 2019. Account-level averages are based on the actual overall contribution and earnings amounts of for these qualified withdrawals on the Ascensus platform for this time period. These account-level calculations assume that no funds are withdrawn during this ten-year time period. Calculations also assume that the account owner is subject to a 10% penalty on market earnings for making a non-qualified distribution and that the taxpayer is in the 24% federal income tax bracket.

Standard Disclosure This illustration is not intended to project or predict present or future value of actual investments or actual holdings, and actual investment returns may be higher or lower than those shown. Past performance is no guarantee of future results.

The tax-deferred difference1

Most are aware all 529 plans are "tax-advantaged," but what do those tax benefits really mean for savers?

All 529 plans benefit from tax-deferred growth, meaning that account balances can grow free of federal and state taxes. Over the long term, this tax-deferred growth can make a significant difference in overall savings. In this illustration, the difference totals more than $6,000 over the course of 18 years.

$100

monthly contribution5%

market return

Years

Making saving more simple

With many competing financial responsibilities, savers can find it difficult to dedicate money to education savings. Automatic contribution options are a convenient way for savers to regularly contribute to their 529 accounts in a way that's simple to manage.

36

%

of account owners making recurring bank contributions

Most savers "set and forget" their automatic investments

In 2019, 58% of 529 account owners that had opted to use automatic investment methods had made no changes to these regular contribution amounts. This suggests that the majority of automatic 529 investors tend to "set and forget" these savings.

As we've seen for retirement savers, optional automatic increase features can boost 529 plan participation and help improve long-term outcomes.

Saving early better prepares families to cover education costs

54% of all 529 accounts on our platform were opened when the beneficiary was 5 years old or younger, with 40% of accounts opened when the child was just 2 years old or younger.

This means that most 529 savers actually have the foresight to get started before their children even begin their first years of school.

Why start early?

Getting an early start is important for families looking to maximize their savings. For families with a beneficiary ages 16 to 17, those that began saving in a 529 account when the child was age 5 or under have 70% more in savings than families who did not start saving until the child was 11 or older.

$47,525

Average balance for accounts opened when beneficiary was under 1 to 5 years old

$36,100

Average balance for accounts opened when beneficiary was under 6 to 10 years old

$28,008

Average balance for accounts opened when beneficiary was 11+ years old

Age-based options help with asset allocation

60% of the accounts in Ascensus-administered 529 plans are invested in aged-based portfolios. This suggests that savers are more comfortable taking a guided approach to 529 investing, opting for help in reallocating savings to a more conservative path over time.

31% of accounts are invested in individual portfolios, managing investment reallocation strategy on their own. However, our data suggests that very few of these investors actively managed their allocations and made fund exchanges in the 2019 year.

Interestingly, 9% of 529 account owners on our platform are invested in both age-based and individual portfolios. This suggests that these investors might have some confusion about the intended use of an age-based portfolio and the fact that it's intended to capture all savings and reallocate them appropriately as the beneficiary ages.

of 529 accounts invested only in age-based portfolios

of 529 accounts invested only in individual portfolios

of 529 accounts invested in both age-based and individual portfolios

Every dollar helps

Many education savers ask the same question: how much do I need to save regularly to make an impact? Our data suggest that nearly three-quarters, or 73%, of 529 account owners save on average $300 or less per month. And, nearly half save on average just $100 or less per month.

These trends support the idea that savers don't have to take an "all or nothing" approach to saving for education. Every dollar saved today is one less that needs to be borrowed or repaid in the form of student loans.

The value of saving versus borrowing

Saving even small amounts in a 529 account over time can help spare families and students from major loan payments in the future. The average account balance for beneficiaries ages 16 to 17 at the end of 2019 was $40,182. How much would it cost a student to borrow this same amount for education?

For that loan amount, the student would be required to pay $10,725 in interest over ten years. That’s equal to over 40% of the original loan amount. In the long run, saving proves to be a much more cost-effective strategy than borrowing.

How much of a college education do average 529 balances fund?

To understand how 529 savings help to pay for an education, we analyzed average account balances for beneficiaries ages 16 through 17 as a percentage of the cost of attending four different types of higher education institutions. On average, these accounts could cover 46% of tuition, fees, and room and board of a four-year, in-state public university, and a fifth of tuition, fees, and room and board of a four-year private university.*

$40,182

average balance for beneficiaries ages 16-17 in 2019

of two years at a community college + two years at an in-state, public university*

of a four-year education at an in-state, public university*

of a four-year education at an out-of-state, public university*

of a four-year education at a non-profit, private university*

% of Tuition Covered by Average Account Balance for Beneficiaries Ages 16-17

Savings are the gift that keep on giving

Now more than ever, families understand the importance of saving for education. With Ugift®, a convenient and free-to-use service, family and friends can gift contributions to a child’s 529 account.

$

273

million

contributed to education savings through Ugift in 2019

20

% year-over-year

increase in total dollars gifted to Ascensus 529 plans from 2018-2019

214

% 5-year growth

in total dollars gifted to Ascensus 529 plans

Enhanced features make 529 gifting even simpler

Since its launch in 2007, our Ugift program has offered 529 account owners a unique opportunity to crowd source their savings efforts.

Ugift now allows users to set up a Gift Giver profile, which allows them to save their banking information, view their gift history, and schedule recurring gifts. Over the course of 2019, we saw over $11,000 new recurring gifts established.

621

,

198

total 2019 Ugift contributions

$

100

median gift amount

11

,

911

recurring gifts established