INSIDE 529 COLLEGE SAVINGS PLANS

As college tuition costs continue to rise, more families are making a long-term savings plan with 529 accounts.

College savings across generations

Average 529 account balances increased across every generation on our platform from 2015 to 2016.

Those under 25 have a significantly higher average 529 account balance than older millennials ages 25-34. This is likely due to the fact that some parents or grandparents have transferred 529 accounts with excess dollars after funding college expenses into the names of the account beneficiaries.

Parents ages 35-44 appear to be considerably increasing their college savings efforts as their kids get older, with an average 529 balance of over $16,000.

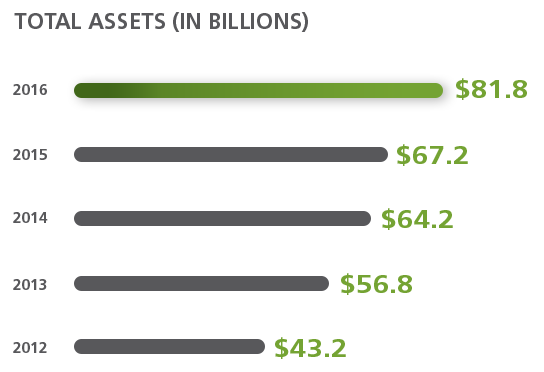

Greater awareness leads to more investors

89

%

increase in 529 account assets on our platform from 2012 to 2016

As more savers have opened 529 accounts and continued to contribute over time, we’ve seen a notable jump in the average account balance across our platform. As of 2016 year end, account owners had an overall average of nearly $22,000 saved versus an average of just $17,000 in 2012.

Younger parents more engaged

Though millennial parents represent a smaller percentage of the overall account owners on our platform, our data suggests that they’re the driving force for new account growth in the 529 market.

When we look at figures from 2011, there were approximately 450,000 529 account owners who had enrolled in a plan between the ages of 25 and 34. In 2016, there were over 800,000 account owners on our platform who had enrolled between those same ages.

362

,

898

new 529 accounts opened in 2016

78

%

increase in the number of account owners on our platform that enrolled in a 529 plan between the ages of 25 and 34 from 2011 to 2016

43

overall average age of 529 account owners on our platform

Employees making college savings automatic

More employees are opting to establish payroll direct deposit into their 529 accounts, making small contributions with each payroll cycle. This approach can make the 529 investment process automatic, simple, and easier to manage over time.

Getting an early start

While Americans ages 25-34 make up less than 7% of savers on our platform, our data suggests that younger parents who open a 529 account early in a beneficiary's childhood often benefit from added time in the market. When is the optimal time to open a 529 account for a child? Let’s do a deeper dive into our platform data to find out.

37% of account owners on our platform enrolled in a 529 plan program when the beneficiary was less than one year old. And over 52% opened a 529 account when the beneficiary was 5 years old or younger.

More parents are starting to plan ahead. And their college savings balances and beneficiaries are reaping the benefits.

37

%

Up to 2 yrs

15

%

3-5 yrs

52

%

enrolled in a 529 program when beneficiary was 5 years old or younger

13

%

6-8 yrs

12

%

9-11 yrs

10

%

12-14 yrs

6

%

15-17 yrs

7

%

18+ yrs

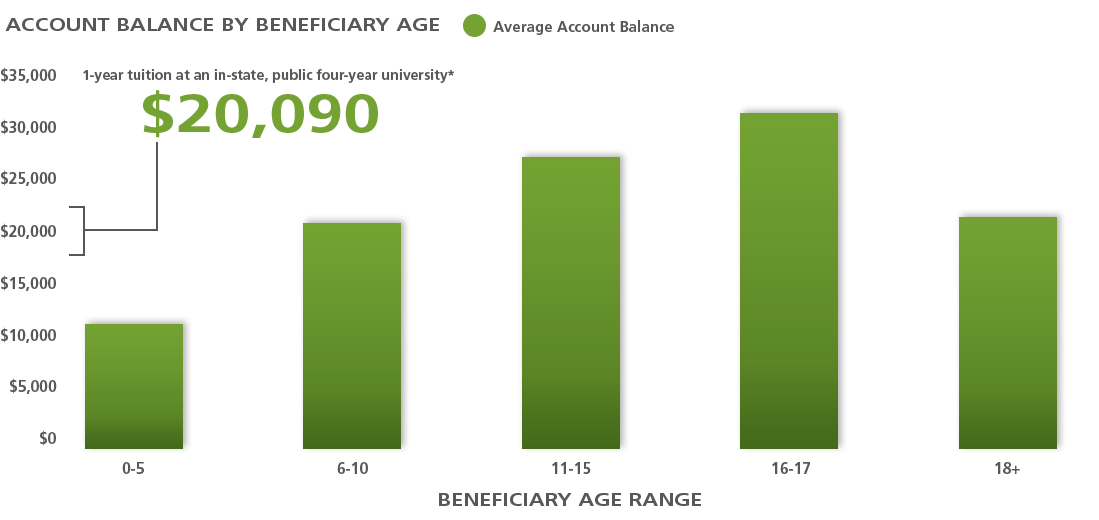

The power of compounding

Families who open an account and start saving early in a beneficiary's childhood are often in a better position to grow their savings. Our data suggests that account owners with beneficiaries ages 16 to 17 who had the foresight to begin saving early have now accumulated an average account balance of $31,460. These savings would cover one-and-a-half years of tuition at an in-state, public four-year university*

Source: Ascensus College Savings platform, as of December 31, 2016.

A joint savings effort

As tuition and college-related expenses continue to increase, Ascensus College Savings aims to make saving for college as simple and convenient as possible. Through the Ugift® service, parents, friends, and family can make meaningful contributions throughout a child’s life toward his or her education.

This easy, free-to-use service enables 529 plan account owners to provide family and friends with a unique Ugift code to make gifting contributions. Friends and family who opt not to use Ugift can also make contributions to a beneficiary's 529 account at any time by personal check.

529 GIFTING CONTRIBUTIONS MADE

Ugift Contributions

Ugift Contributions

$109,560,000

total Ugift contributions in 2016

$361,370,000

Ugift contributions since the program's inception

$100

median Ugift contribution amount for 2016

In the last 5 years, Ugift contributions have increased by over

500%

.

529 investors favor age-based investment options

Our data suggests that, like many retirement savers, 529 account owners seem to prefer a guided, low-maintenance investment strategy. Individual portfolios within a 529 plan are defined as standalone, static investments in which an account owner opts to build their own allocation. However, with age-based portfolio options, the 529 program manager handles asset allocation and moves the funds along a glide path as the beneficiary nears college age.

57

%

of total assets invested in age-based options

43

%

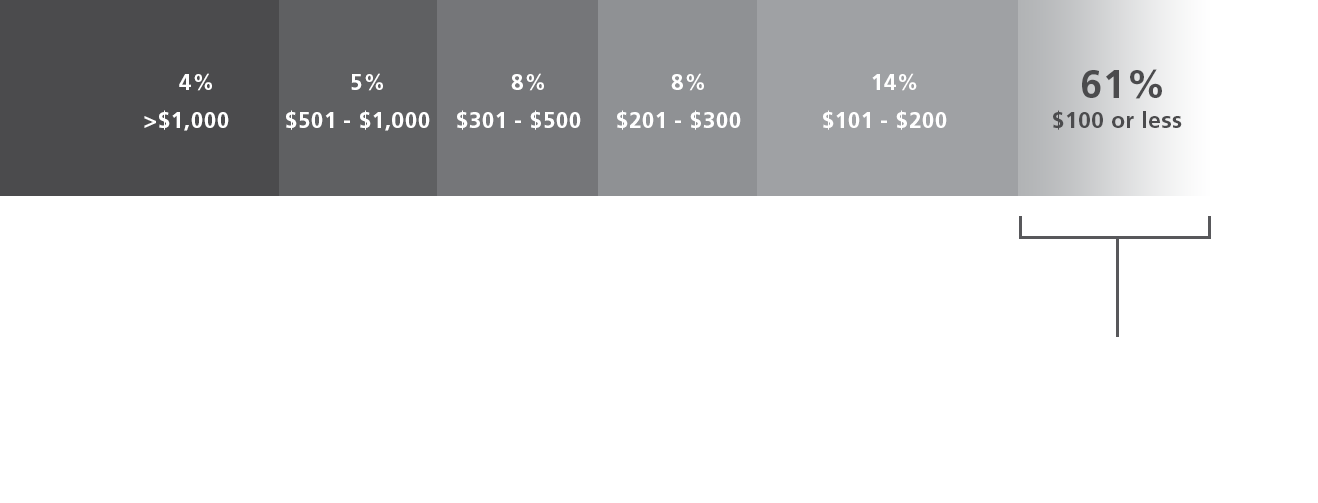

of total assets invested in individual portfoliosSaving modestly over the long term

Our 529 platform data shows that savers don’t have to take an "all or nothing" approach to saving for education. Savers can evaluate their family’s situation and plan their strategy accordingly. Most 529 account owners opt to make smaller contributions of $100 or less more frequently over time.

% of total contributions

Tracking progress as college nears

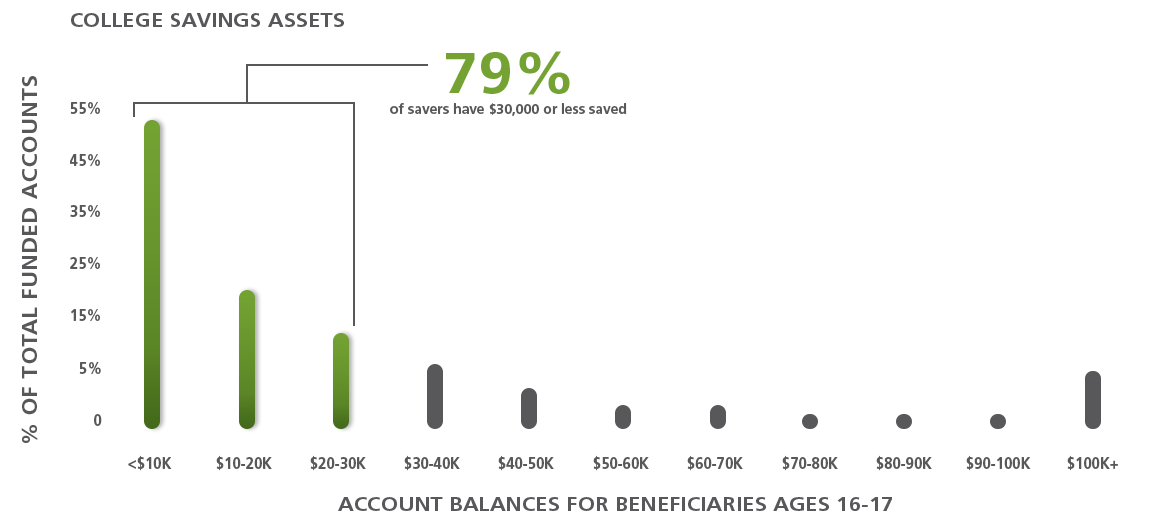

The chart below provides a more detailed look at accounts held for beneficiaries ages 16-17. This is typically when accounts are at their largest—before account owners start withdrawing to pay for education expenses. Approximately 80% of these account balances were less than $30,000 as of December 31, 2016. However, the overall average 529 account balance for savers with beneficiaries approaching college age is trending in a positive direction at over $31,000. That’s $31,000 less that the student or family will need to borrow in order to cover college costs.

How much is enough?

The average annual cost of an in-state public four-year university during the 2016-2017 academic year was just over $20,000; the average annual cost of a four-year private university was over $45,000.* How much of these four years of tuition do college savers have covered?

Non-profit, four-year private university

17

%

Out-of-state, public four-year university

22

%

In-state, public four-year university

38

%

Two-year community college + In-state, public two-year university

48

%

Here, we analyze current account balances as a percentage of different tuition mixes for beneficiaries approaching college age. This group might only have 17% of a four-year private school covered, but they also have 38% of tuition for a four-year public school education saved.

For parents and families looking to learn more about covering rising tuition costs, howtosaveforcollege.com provides the basics on 529 plans and features a college planning calculator. This site provides users with the resources and information they need to formulate the right strategy to help meet their savings goals.

Source: Ascensus College Savings platform, as of December 31, 2016.

Account owners making their savings last

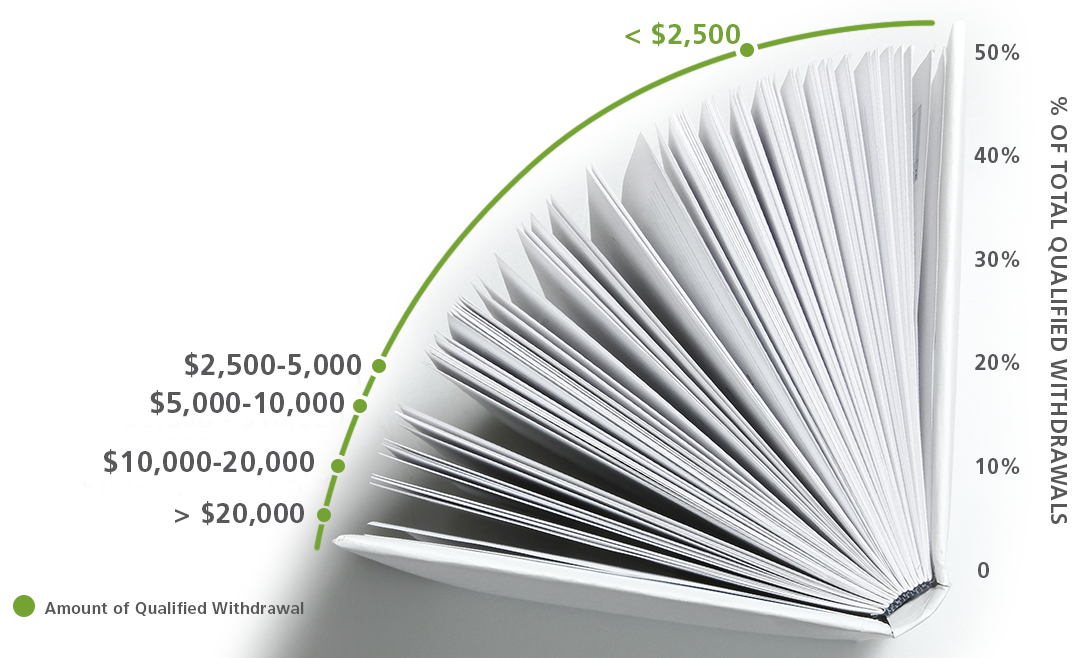

During 2016, Ascensus College Savings processed over 945,000 distributions that account owners identified as "qualified withdrawals." These are disbursements from 529 plan accounts to cover tuition, room and board, and other higher-education-related expenses allowable by Section 529 that qualify for federal tax benefits.*

Over 50% of these qualified withdrawals were for $2,500 or less. This trend suggests that most families are putting their college savings to work in small increments over time, rather than using these savings all at once.

*The availability of tax or other benefits may be contingent on meeting other requirements.