INSIDE AMERICA'S RETIREMENT PLANS

While most retirement savers are behind on their goals, our data suggests that smart plan design can make all the difference.

Retirement savings across generations

Year over year, the average 401(k) account balances across most age segments have increased.

Between the 35-44 and 45-54 age ranges, retirement savers are adopting a more proactive approach, with the average account balance of this younger bracket nearly doubling to over $63,000 as they gear up for their 50s.

How much is enough?

Most Americans are unsure about how much to save from their pay. We analyzed average deferral rates across generations to determine how much savers have decided to put away.

Young millennials under the age of 25 have the lowest overall average deferral rate at just 3.2%. It's likely that they're not saving as aggressively because they're still young and know that retirement is decades away.

While we see savings rates continuing to increase steadily as savers age, the average deferral rate across all generations still appears to be surprisingly low at just 5.5%.

How can advisors and retirement plan sponsors encourage a boost in plan deferral rates? Employee education and financial wellness tools can make a major impact. Ascensus' targeted communications are personalized and mailed directly to employees, illustrating what their savings decisions today will mean for their retirement nest egg tomorrow. In 2016, employees who chose to enroll in their company retirement plan after receiving a targeted communication deferred, on average, 6.24% of their pay.

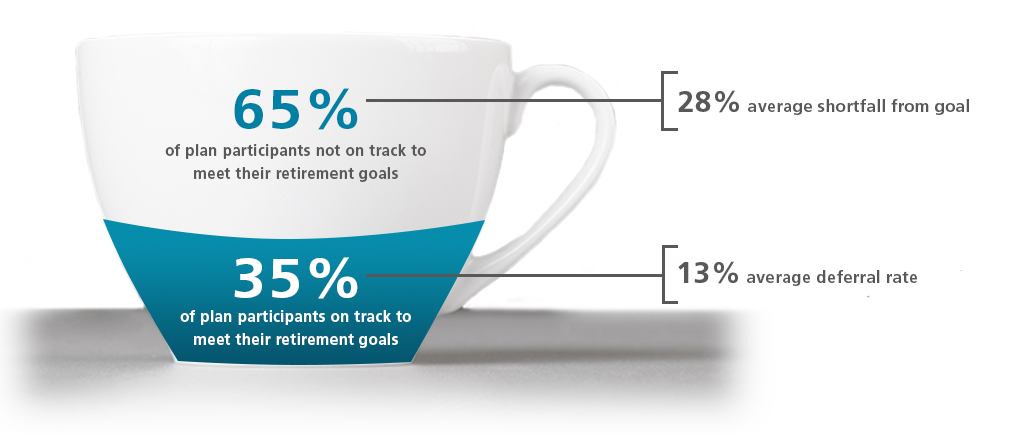

Awareness is the first step

According to our Retirement Outlook Tool, only 35% of employees are on track to meet their retirement goals.

However, once savers become aware of their shortfall, they often take steps to increase their retirement savings efforts. In fact, 55% of participants who weren't deferring to their plan at all started contributing at an average rate of 8% after using the tool.

Match creates incentive to save

By designing a plan that motivates employees to start saving, employers can play a major role in contributing to overall retirement readiness.

Retirement plan sponsors on our platform are stepping up to the plate, with 81% of them opting to fund a match, versus just 69% at 2015 year end.

73

%

of employees indicate that an employer match motivates them to save*

81

%

of plans on our platform fund a match

18

%

higher average participation rates for plans that fund a match versus those that don't

Digital enrollment boosts plan participation

Digital enrollment simplifies the enrollment process for employers and employees, and a higher percentage of our clients are offering it than ever before.

We continue to remove the roadblocks, now offering quick and easy mobile enrollment that can be completed in as few as three taps.

92

%

of plan sponsors offering digital enrollment

millennials driving increased usage of digital and mobile enrollment

Source: Ascensus platform, as of December 31, 2016

Making saving automatic benefits employees and the plan

We've tracked participation rates across plans converting to Ascensus from other plan providers and found that, on average, these plans had a 64% participation rate.

Plans that opted for auto enroll on our platform saw significantly higher average participation rates than those not using auto features. The highest average plan participation was found in plans that had both auto enroll and auto increase at just north of 80%.

69%

rate for plans without auto enroll

78%

rate for plans with auto enroll

80

%

rate for plans with auto enroll and auto increase

Employees likely to follow their employer's example

Automatic features have proven very effective in helping combat one of the most common retirement savings hurdles: procrastination. But how many employees are staying the course once they've been auto enrolled in their employer's plan? For employers that opted to auto enroll their next new hire at a default rate of 3-5%, a significant number of employees chose to stay enrolled in the plan.

stay enrolled at the default rate

increased their savings rate

Employers and advisors continue to favor low-cost funds

Over 61% of funds available on our platform generate 0-25 basis points (bps) in revenue*. Nearly 50% of the zero-revenue-generating funds available on our platform were utilized by advisors in 2016 versus just 33% of the 1-25 bps revenue. This suggests that an increasing number of our advisor partners and their clients are seeing the value in our low-cost, quality investment options.

of funds on our platform generate 0-25 bps in revenue

of zero-revenue-generating funds available were utilized in 2016

Retirement wellness by industry

Offering employees a plan for the future

By offering a quality retirement plan, companies can attract and retain top talent. Businesses in the following industries accounted for the majority of plans on our platform, suggesting that they have a specialized focus on retirement readiness and competitive employee benefits programs.

|

Professional, Scientific, and Technical Services |

|

Healthcare and Social Assistance |

|

Manufacturing |

|

Finance and Insurance |

Top industries for savings progress

There is a strong correlation between average compensation and average 401(k) account balance on our platform. Employees in the following industries have made the most progress toward their savings goals.

|

Finance and Insurance |

|

Professional, Scientific, and Technical Services |

|

Mining |

|

Wholesale Trade |

Top participation rates

Not surprisingly, employees in the finance industry who are most likely more aware of the need for financial wellness have the highest overall average participation rate.

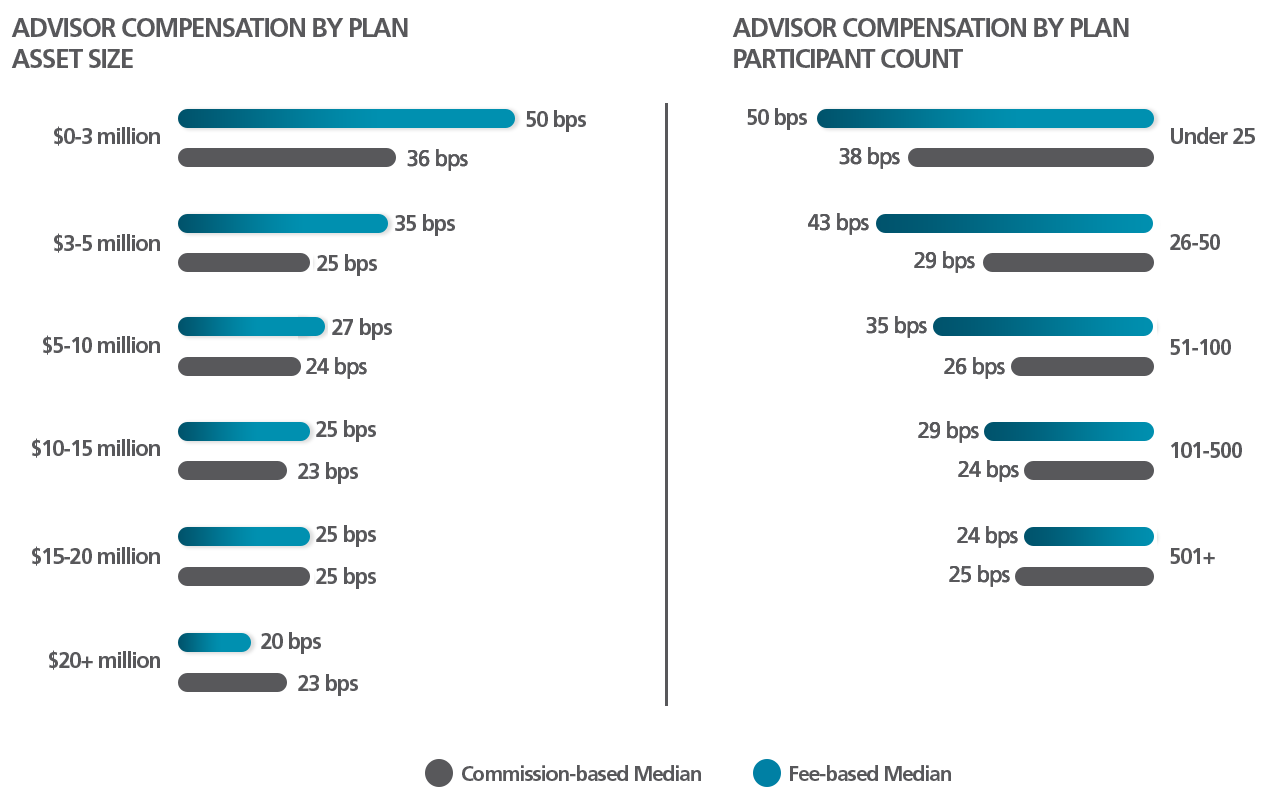

Tiered basis points become more popular choice

From 2011 to 2016, the most commonly used advisor compensation method remained flat basis points; however more plans are electing a tiered method. With a tiered approach, advisors can demonstrate to their clients that the advisor's compensation proportionately decreases as a client's plan assets increase. These advisors therefore don't have to reprice or renegotiate as often because they've built a fee schedule that allows them to systemically reduce their average compensation. Ascensus has seen a 4% decrease in the usage of flat basis points, most likely due to more advisors shifting to a tiered approach.

| Flat Basis Points | Tiered Basis Points | |||

| 2011 | 2016 | 2011 | 2016 | |

| 91% | 87% | 4% | 8% | |

| Total | ||||

What are your peers charging?

In light of regulatory developments and the need for pricing transparency, more financial advisors are considering the shift to a fee-based service model. How are commission-based and fee-based advisors pricing their services in today’s landscape?