A snapshot of retirement readiness

Account balances on our platform across all generations are likely lower than what would be required to cover retirement goals. But it’s important to note that some of these savers have additional assets saved in IRAs or external savings accounts.*

To get a holistic view of progress, savers should aggregate their balances across the various funding sources they plan to leverage in retirement.

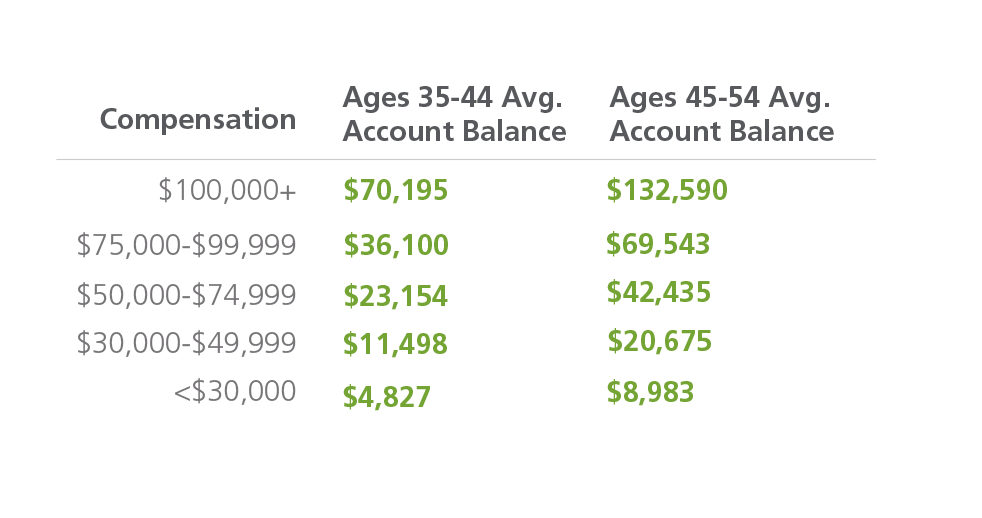

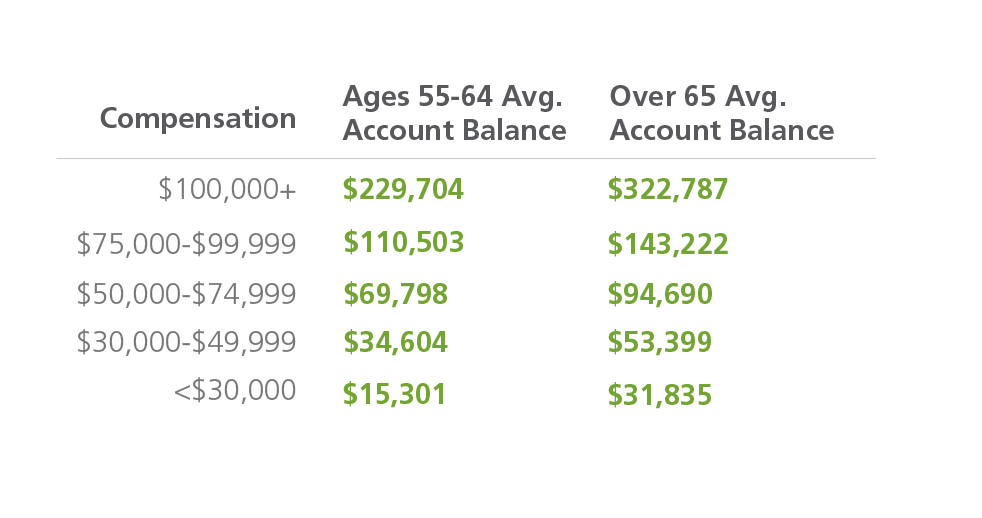

Savings progress across generations

Our Retirement Outlook Tool allows savers to refine retirement savings goals. It illustrates for users how their current reality compares to their expectations for the future.

How much progress have savers of different generations made toward their goals?

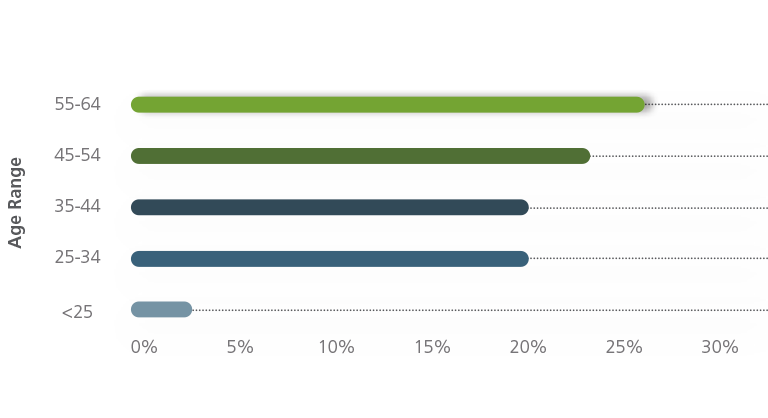

% of Savers on Track to Meet Goals

Savers in the 45 to 54 age group were the most likely to be on the right track, with nearly 25% finding that they were saving adequately to meet their goals. However, individuals under age 25 had the most work to do, with 97% falling short.

Smart technology boosts awareness of shortfalls

While our data suggest that savers across all age ranges might need to ramp up their contributions, there is a bright side. Awareness seems to be the first step in the right direction.

26%

of users started contributing for the first time after using the Retirement Outlook Tool8%

average savings rate selected after using the toolDownload the complete Inside America's Savings Plans report

DownloadAuto features remove the roadblocks

Automatic enrollment and automatic increase features make it as effortless as possible for employees to start contributing to their 401(k). Plans with auto enrollment have participation rates 10% higher than those without. Employer matching contributions offer additional motivation and an even more notable boost in plan participation when coupled with auto features.

70%

average participation rate for plans without auto-enroll80%

average participation rate for plans with auto-enroll81%

average participation rate for plans with auto-enroll and auto-increase84%

average participation rate for plans with auto-enroll and auto-increase that fund a matchRetirement plan engagement by industry

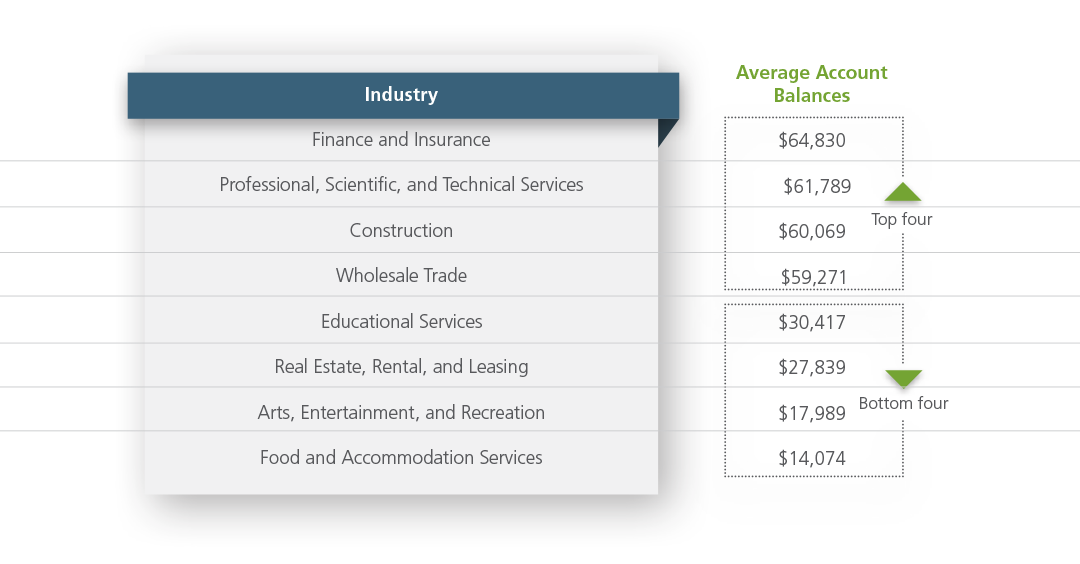

Employers across a diverse range of industries have stepped up to the plate, offering a retirement plan to help their employees achieve a more financially secure future. But how are employees across these different industries engaging with their 401(k) plan?

Across our platform, retirement plan participation is highest among employees in the finance and insurance industries. Employees in these industries are likely somewhat knowledgeable on financial wellness and therefore understand the importance of saving for retirement.

It's important for financial advisors to consult with clients that might fall into lower-engagement industries to discuss how incorporating auto features or other plan design elements might drive better outcomes.

Making the most of their retirement plan

Employees in the finance and insurance industry have the highest average account balances at $64,830, with professional services industry employees in close second. Again, it's important to note that these balances reflect only those assets saved in these employees 401(k) accounts on the Ascensus platform. It's highly possible that these accounts represent just one piece of these savers retirement planning puzzle, with IRAs, standard savings accounts, or additional investing accounts also playing a role.

How do employers pay their plan fees?

72

%of employers elect to be invoiced for recordkeeping fees*

28

%of employers pay their recordkeeping fees using plan assets*

Employers who pay "out of pocket," writing a check for recordkeeping services, under a fee-based structure receive the benefit of a business tax deduction for that expense. And by opting to pay out of pocket, employers can also enable assets to grow and help boost the plan’s market value over time. Consider the following example.

For a full-service plan with:

25

participants$75,000

in annual contributions5%

market growth$3,950

annual recordkeeping fee

By paying out of pocket over the course of 10 years, the plan experienced over $56,000 in a market value differential because plan assets remained in the plan and benefited from compounding.

This illustration is provided solely as an example based on the assumptions and plan information highlighted above. This is an estimate only and is not a guarantee of any particular results. Actual results may differ. This illustration is not intended to be investment advice or a recommendation to purchase, sell, or hold any investment. Ascensus assumes no liability for use of this illustration by any third party.

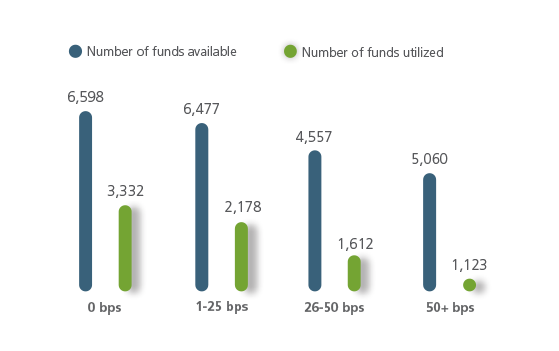

Advisors and employers continue to focus on value

Investment providers have also evolved their offerings in response to the need for lower-cost solutions that can enable employees to more affordably invest their savings. Employers have seen a new influx of low-cost investment options.

Our data suggest more and more financial advisors are guiding their clients to use low-cost share classes that can deliver better value for the plan.

Fund Utilization Breakdown by Service Revenue*

*Service revenue is defined as sub-TA plus 12b-1 fees for purposes of this analysis.

Additional retirement assets accumulate in IRAs

Individual Retirement Arrangements (IRAs) are another type of tax-deferred account that have been a primary retirement savings vehicles for individuals over the past several decades. At Ascensus, we administer over 1.4 million Traditional and Roth IRAs, which gives us insight into how the modern saver is using these vehicles to supplement other sources of retirement funding.

2

.8

billion in Roth IRA assets

$

13

,300average Roth IRA balance

$

26

.1

billion in Traditional IRA assets

$

27

,700average Traditional IRA balance